POSTED BY ANGUS GEDDES

Bull markets die on euphoria and not much else. So until we see that psychological dynamic playing out in spades, I’m inclined to “disengage from the herd” and stay with the primary trend.

How many participants have been scared out of the markets this year? Climbing the wall of worry is what the bull does. So by definition, the bull will take as few “rodeo riders” as possible. Hanging on is the key.

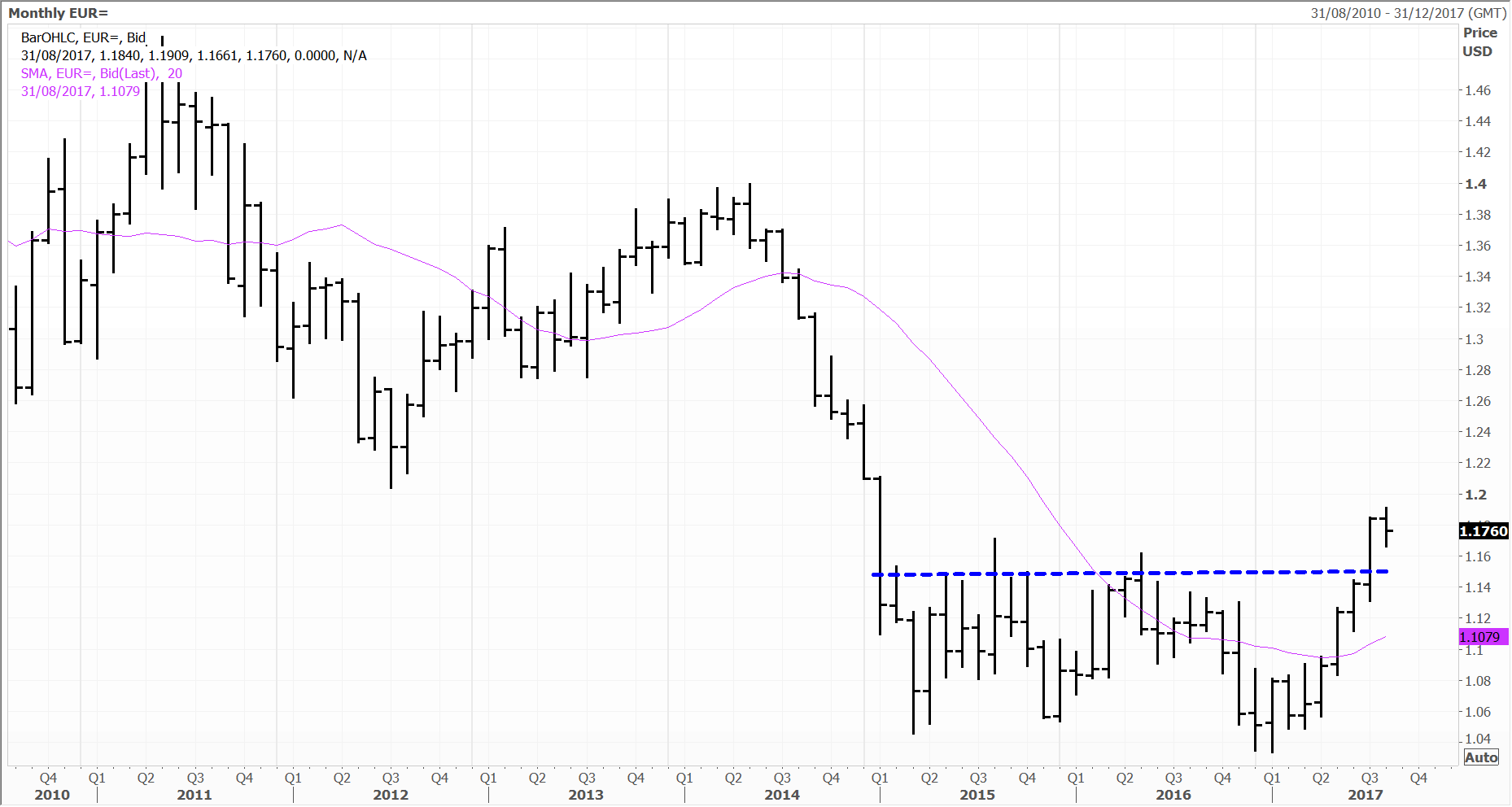

US Treasury yields and gold prices lost ground on Tuesday and fell ahead of the Jackson Hole central bankers summit this weekend. Federal Reserve Chair Janet Yellen and European Central Bank President Mario Draghi will be closely watched amongst the speakers.

I think it will be very interesting in terms of what Mr. Draghi has to say; particularly given the euro (chart below) has rallied to the highest level in a few years. The US dollar index rallied 0.5% to 93.5 ahead of the summit.

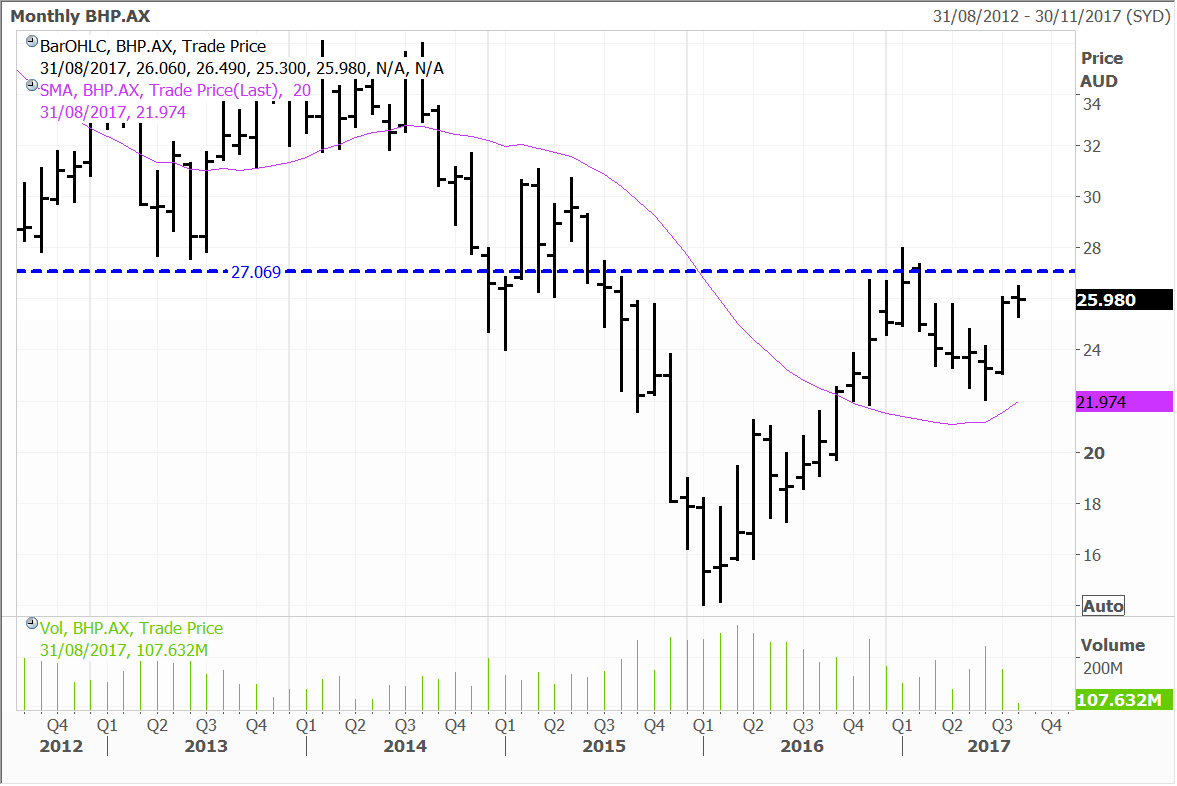

There have been several blue-chip misses in the reporting season thus far, but one theme that has been prevalent as we expected, is commodity price strength. This has been evident in the results from the big miners, and was again on display in a robust full year result from BHP on Tuesday.

BHP shares rose 1.1% as the company reported a full year net profit of US$5.89 billion versus a loss of US$6.385 billion a year ago, underpinned by the iron ore division. Underlying attributable profit more than quintupled to US$6.732 billion, while revenue rose 24% to US$38.285 billion. BHP more than tripled its 2017 final dividend from to US43 cents a year, bringing the value of full-year dividends to $4.4 billion.

EPS of $1.10 was a miss on consensus average expectations of $1.35, but clearly ever strengthening commodity prices and the sale of the US shale business have bolstered the outlook further. Shareholder returns are set to accelerate, with more cost cutting, and robust commodity prices setting the stall for BHP to generate around US$10 billion of free cash flow in fiscal 2018.

BHP is testing historical resistance at $26. Further strength in commodity prices will be the probable catalyst for the stock to punch through into a new trading between $26 and $28.

BHP has put its shale business on the block, after admitting it made mistakes in the foray, and also under some pressure from activist US hedge fund Elliott Associates. This could fetch around US$10 billion, and would see capital initiatives (buybacks or alternatively a special dividend) on the agenda, and further improve an already strong balance sheet. This will be a welcome liquidity boost, although I am not sure that now is the time to be achieving the best possible price. In any event a bird in the hand…

Either way, BHP will maintain tremendous leverage to ongoing strength in commodity prices. These have also increased significantly post the year end, with iron ore alone rising 50% in the last 50 days, and pushing US$80 a tonne. Copper and zinc as other examples remain around 3 and 10-year highs respectively.