POSTED BY ANGUS GEDDES

Good morning,

US stocks rebounded on Wednesday after the Fed left interest rates on hold, but signalled ‘further’ tightening to come this year. It was also a big day for quarterly earnings, with several key companies reporting strong results. The Dow Jones rose 0.28% to 26,149, the S&P500 edged up 0.05% to 2,823, while the Nasdaq was 0.12% higher at 7,411.

Tech stocks were amongst the strongest performers while Boeing rose to a record high after quarterly earnings surpassed Wall Street’s expectations. The aircraft maker is the heaviest weighting in the Dow Jones and expects to hit a new delivery record in 2018. Precious metals stocks were also well bid.

While continuing to echo a cautious tone, there were some subtle changes in the language used by the Fed following the meeting, which has all but locked in a rate hike in March when Jerome Powell takes over as Chair. We went on the record calling for at least four rate hikes by the Fed this year (with the markets pricing in two or three), and this scenario has now become more likely.

Janet Yellen has bowed out gracefully and in ‘passing the baton’ has set the scene for Jerome Powell to pick up the pace on rate tightening.

The statement from the central bank read that “The committee expects that economic conditions will evolve in a manner that will warrant further gradual increases in the federal funds rate.” It was notable that the FOMC added the word “further” twice to previous language.

The Fed left the benchmark interest rate unchanged as expected in a range of 1.25% to 1.5%, but said it anticipated inflation will rise this year, which clears the path for a series of rate hikes under Jerome Powell. Strong employment, solid capital investment and consumer spending are expected to see the economy grow at a moderate pace in 2018.

Regarding the central bank’s 2% medium term inflation target, the FOMC stated, “Inflation on a 12-month basis is expected to move up this year and to stabilize.” Now into the ninth year of economic expansion following the GFC, the Fed is still focused on stimulating growth, in part because inflation has remained stubbornly low.

This though is all about to change though in our view, and this is also why we are witnessing something stirring in the bond market (see further down). The yield on the 10-year Treasury ticked up at one stage to 2.74%, up from 2.72%.

We believe that inflation is going to heat up and force the Fed to raise rates faster than the markets expect. As I wrote earlier in the week, I believe that US interest rates have passed a “generational inflection point”.

Elsewhere, in Donald Trump’s first State of the Union address since becoming President, he urged Republicans and Democrats to work together towards compromises on immigration and infrastructure and implement legislation that generates at least $1.5 trillion for new infrastructure investment. This will be Trump’s next key focus after pushing through the biggest overhaul in the US taxation system since the 1980s.

Trump will now aim to shore up support with Republican conservatives, but stick to his election promises of building the border wall with Mexico and restricting immigration laws. He has a chance of being successful with some of these policies, especially in my view the $1.5 trillion infrastructure spending. This is not because I believe in Mexican border wall, but because much of the US infrastructure is badly dilapidated and in need of an upgrade.

Whilst the markets have rallied, and investors have priced in the benefits of the tax cuts looking ahead one to two years out, the infrastructure spend has been off the radar. If Trump were to look as though he could succeed in getting the infrastructure bill passed through congress, Wall Street would likely have another leg up later this year and end December on another strong note.

I can’t get too negative on a potential selloff in US and global stocks near term and see this as being strictly limited to a 5% to 10% correction at best. US, Asian and European corporations are all reporting the best earnings in some time. As is Australia’s resource sector. Whilst the expensive US and global tech sector is prone to a selloff – and we could still see any disappointment amongst the leading technology companies as being the catalyst for a steep fall – I think this will prove short lived near term if it eventuates.

Rising bond yields are a concern. However, at this stage in the cycle, stocks are less prone and exposed than the bond market, because a 1% rise in yields on a 10 Year Treasury would induce a significant drop in the capital value, but the S&P500 would still be attractively priced on a relative basis.

Breakout in 10 Year T Bond yields? Almost – wait for inevitable reversal that should come at any time and for the bid to come back into bonds, but I would say this market is ripe for picking now in terms of going short. We have not yet shorted US bonds or any other bond market for that matter – but we have shorted expensively priced interest rate sensitive stocks a while ago and will add to this position. I am intending to short selected bond markets (which price off the US) in due course. It’s really only a matter of timing now.

10-year US treasury yields

We have said that by the end of this year if the US economy remains on measure, popularity for Trump will swing in his favour from his current very poor standing in the polls. This is a contrarian view, but I think which has foundation. Trump has already galvanized market support on Wall Street, which has positively priced in his tax cuts. And the pendulum may already be turning. According to one report on Bloomberg, a CNN/SSRS snap poll said “48 percent of those surveyed had a “very positive” response to the speech and 22 percent were “somewhat positive.”

So green shoots are already emerging for the President, and I only mention this – not because of my personal politics – but because the markets will welcome this!

Trump also mentioned in his Union address that he was “extending an open hand for an immigration deal and that he would provide Dreamers a pathway to citizenship over 10 to 12 years in exchange for funding the border wall”. I think he is lining up his next “deal on Capitol Hill”.

The President labelled his plan a “down-the-middle compromise“. Like him or hate him, he is establishing himself as a ‘reformer’ and the markets are going to see this as being very much pro-business. I see Wall Street finishing higher this year, despite the superstitions around years ending in 8, because of the positive disposition to American business that Trump politics hold.

Of course, Trump “took credit for the economy, the rise in the stock market, and a low jobless rate”. He also somewhat boasted about the economic growth he believes will result from tax cuts Republicans pushed through Congress late last year. But you can’t deny that the tax cuts are not going to have a positive impact over the medium term on the US economy.

If Trump is successful in pushing through the infrastructure package – and I believe he will get there this year – then that in itself becomes yet more fiscal stimulus for the US economy, which in turn is going to drive up corporate earnings.

There is definitely a risk that everything in the US overheats and we have laid out our case some time ago, as to why US interest rates are going to rise this year. But for now any correction should be viewed as a buying opportunity because the underlying earnings growth momentum is intact and looks to not be slowing anytime soon.

Trump said in his address that he would like a compromise over a plan to rebuild aging roads, bridges and other infrastructure. He also said he wanted legislation to generate at least $1.5 trillion through a combination of federal, state and local spending as well as private-sector contributions. I think both the Democrats and Republicans understand the need for the US to upgrade. So a potential deal is on the table for later this year.

Back to the market moves, technology companies, including Software and semiconductor stocks were among the strongest performers and ahead of several tech bellwethers reporting later in the week. Boeing rose 5% after quarterly earnings beat the Street. Gold and commercial real estate stocks were also rising. Traders were also selectively looking for relative ‘bargains’ after recent softness. The weakness in healthcare continued as investors fret about whether Amazon will be able to disrupt the industry.

As is wrote yesterday, Amazon is teaming up with Berkshire Hathaway and JPMorgan Chase to create a company that to provide their employees with quality health care at a reasonable cost. The venture is only in the early planning stage though.

Asian stocks were generally steady on Wednesday after the falls on Monday and Tuesday, although Japan’s Nikkei was lower mainly on profit taking. The Bank of Japan firmed up rhetoric to dispel market speculation of an early withdrawal of the current stimulus program and boosted central bank bond purchases on Wednesday, as well as reassuring the markets that monetary policy would remain ultra-loose given the low inflation rate.

There had been a reaction in the markets to BOJ Governor Haruhiko Kuroda recent speech at the Davos conference where he inferred that Japan was getting closer to achieving the 2% inflation target.

However, his deputy Kikuo Iwata stressed on Wednesday that the bank would “maintain powerful easing” with inflation far from its 2 percent target. Iwata blamed “market misunderstanding” of BOJ policy for driving up the yen more than he expected, saying investors were wrong to assume the central bank will soon raise rates.

Mr Iwata went on to say that “if economic conditions change, it’s important for the BOJ to be ready to adjust its yield targets looking at economic prices and financial developments. But we’re not in a situation to change our yield target levels now and I don’t expect any changes for the time being.”

A summary of BOJ policymakers’ opinions, released yesterday, quoted one of them as saying at January’s rate review that a rise in market expectations for an imminent departure from monetary easing would be “undesirable”.

However, as I have been writing in these notes Japanese Government bond yields are pressuring significant historical overhead resistance on the charts – see below. It won’t take much further upside in 10 JGB yields to pierce major historical resistance. So it seems the BOJ is jawboning (and acting) on one hand to contain yields, but the market is pushing in the opposite direction.

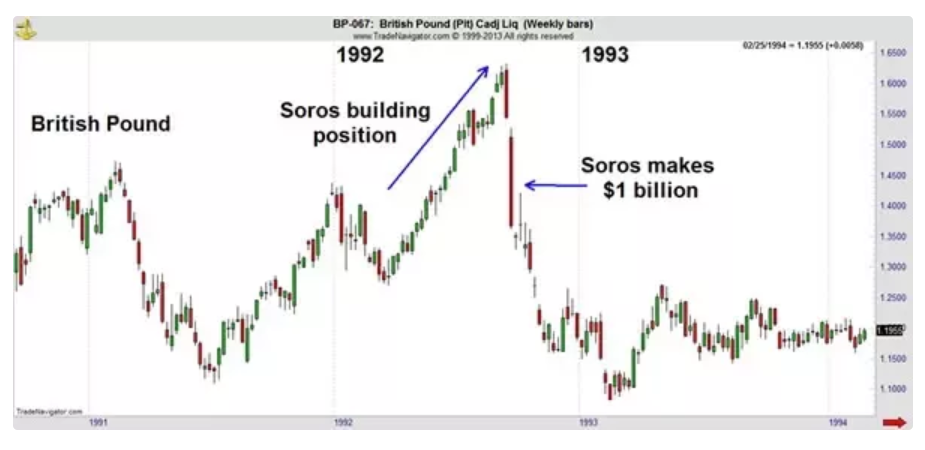

We have seen this game of “tug and war” before with the central banks and the markets. George Soros famously broke the Bank of England when he shorted the pound against the central banks’ concerted buying efforts (which failed!) to hold the currency up. We are long – the (long dormant) Japanese financial sector – which will be a principal beneficiary of higher rates. I note that yesterday factory output grew in December at the fastest pace in eight months on robust global demand for Japanese goods.

Just how did George Soros break the Bank of England?

Under the BOJs current yield curve control (YCC) policy (NIRP) – short-term interest rates are at negative 0.1% and the 10-year government bond yield is around zero percent – it is a very difficult environment for Japanese banks to make money. I think this aspect of the BOJ’s policy has to change and it is only a matter of time before it does.

Iwata is seen as an architect of the BOJ’s huge asset-buying or quantitative easing programme that aimed to shock the public out of a deflationary mindset. Having been in Japan recently for research (and some superb skiing) I was shocked at how packed the shops, department stores and malls were with emboldened consumers eager to spend. The mood has changed definitively and I am a huge bull on the Japanese economy and the Japanese stock market – which we have backed heavily in our funds management operations.

The Shanghai Composite edged down 0.21%, erasing the gains seen in morning trading after small-cap companies were hit hard following comments from a regulator about clamping down on speculation. Small-cap companies listed in the mainland are very much retail dominated, with momentum trading often a key factor determining the fate of their stock prices.

China’s Purchasing Managers’ Index (PMI) came in at 51.3 this month, which was lower than expected (51.5), but still above the key 50 mark, with anything above that line indicating expansion. It was the 18th straight month the PMI indicated expansion. Non-manufacturing (i.e. services) PMI came in at 55.3, beating the forecast of 54.9 and up from 55.0 the prior month.

Praemium has also been a strong performer for us, with similar thematic drivers. The shares were 5% lower yesterday, but it is probably not surprising to see some profit taking given the run the shares have had. The outlook though is still strong, and the recent addition of international securities to the SMA proposition in Australia will further bolster the company’s competitive advantages. Praemium’s international business also continues to offer robust turnaround potential following some strategic shifts and savvy acquisitions. We hold Praemium in the Concentrated Australian Share and Small/Mid-Cap managed account portfolios.

Praemium

Hong Kong-listed shares of Wynn Macau clawed back some ground lost following sexual misconduct allegations against billionaire Steve Wynn that came to light last week (which he denies). Wynn Macau shares gained 3.4% and the broader market is set to benefit hugely from wave of outward bound mainland China tourism over the next decade.

Gaming revenues in Macau have been outpacing broker forecasts. The primary risk to the likes of Wynn Macau and Nasdaq-listed parent Wynn Resorts is that Steve Wynn is forced to step away from the CEO role at the company and in the worst-case scenario the casino licenses are put at risk. As I wrote yesterday, I don’t believe there is a risk to the license regardless of the outcome of the allegations. Fat Prophets holds an overweight exposure to Macau in the Global Contrarian Fund and our Managed Account portfolios via Wynn Resorts, Wynn Macau, Sands China and MGM China.