POSTED BY ANGUS GEDDES

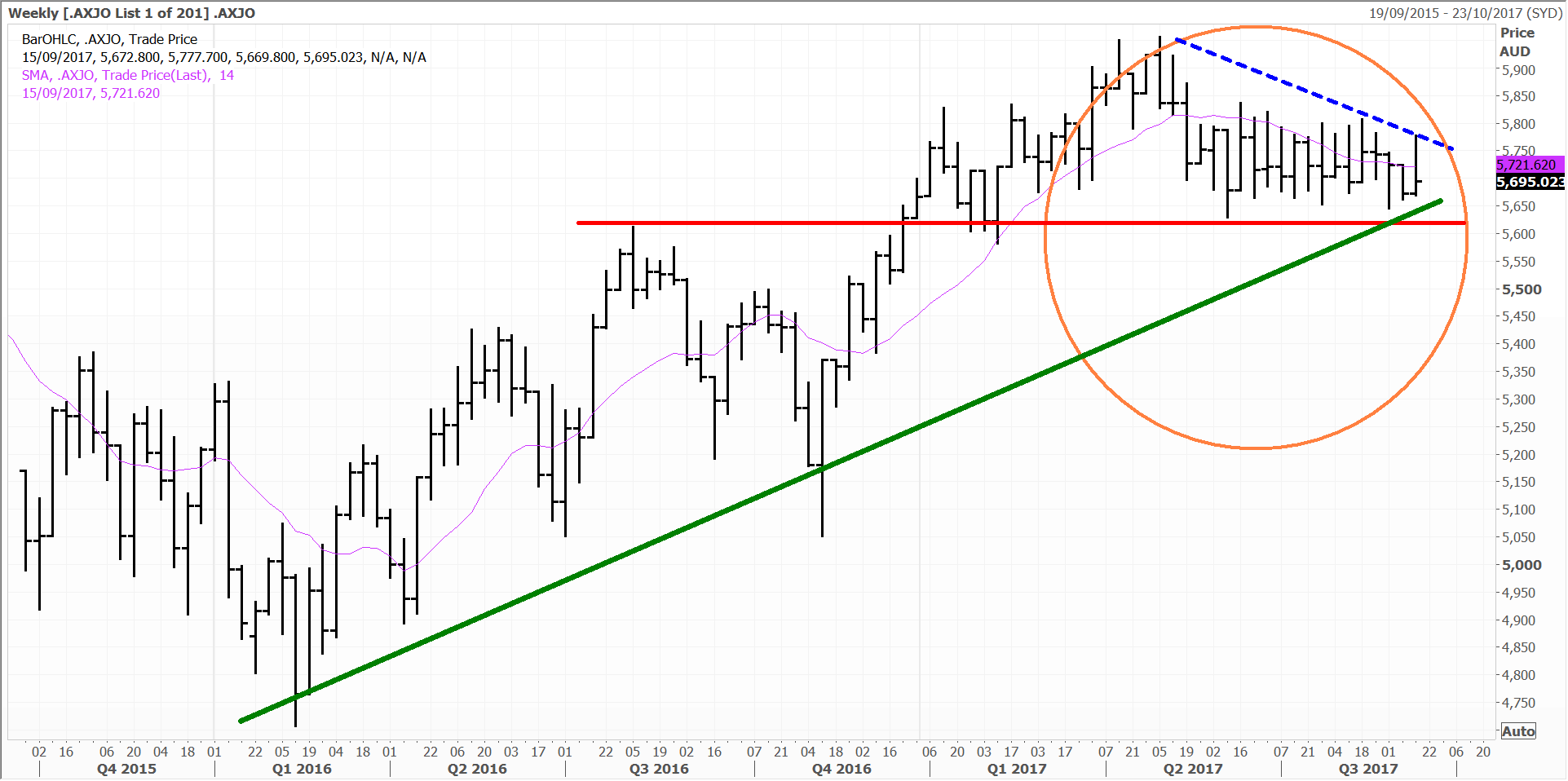

In Australia the market fell on Friday, with the ASX200 closing the session down 43 points at 5695. The index nonetheless posted a gain of 0.4% for the week, and I think there are legitimate reasons why a decisive break away is only a matter of time – see below. A key driver will be the resources sector, which has performed consistently, but has much more upside in our view, particularly if commodities can hold existing price levels, or even push higher as inflation comes through the system.

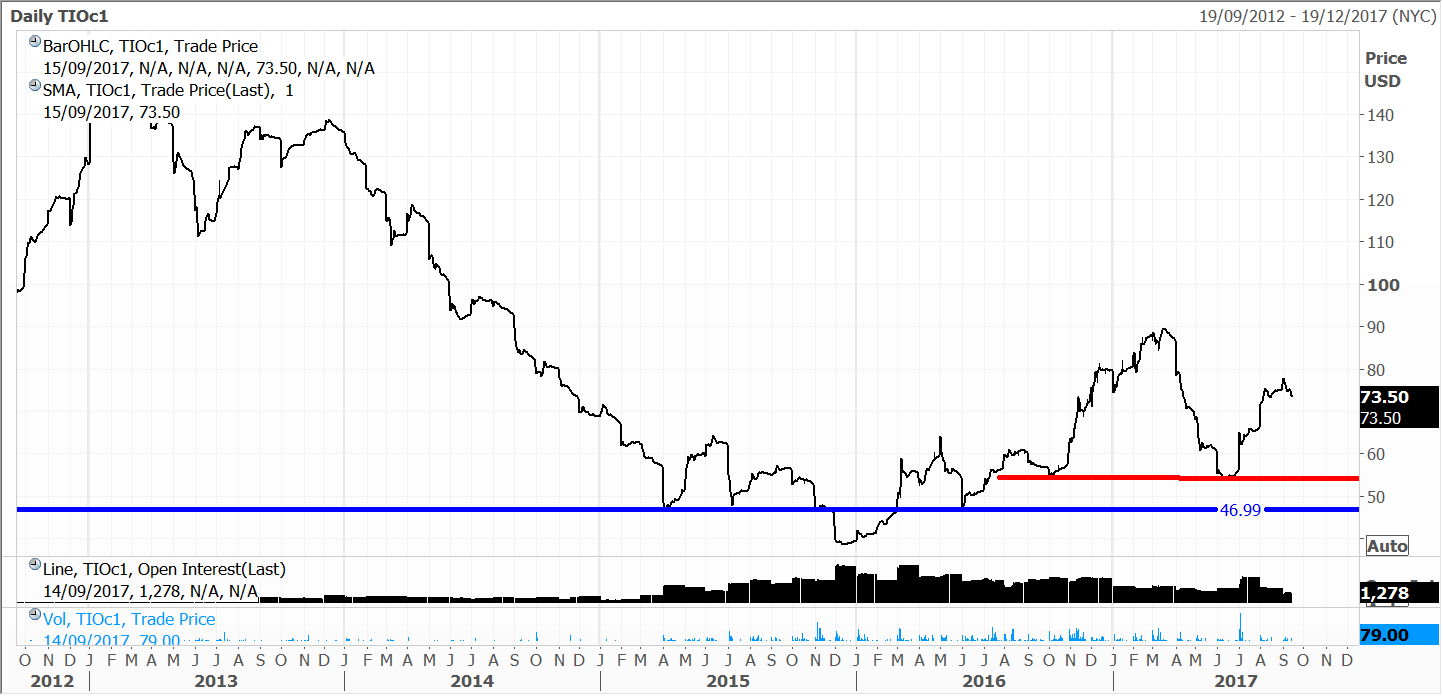

This will be to the consternation of the resource bears, and even the majority of institutional analysts, who have forecast significantly lower price targets for iron core, copper, and a host of commodities across the spectrum.

“Beat’em or join’em”. It is interesting that several investment banks have called for a correction in the resources space over coming months. The risks of a relief rally in the US dollar have increased, and this could be a headwind for the resources sector near term, but not looking out further into 2018.

A number of investment banks were forecasting iron ore to fall below US$50, but we think this is unlikely, with a major bottom being formed in 2015 and a subsequent successful test of support earlier this year.

On this note HSBC has issued a report concluding that iron ore pricing will experience a “correction” in the last three months of 2017, and then fall below US$60 a tonne in the first half of next year as China clamps down on steel production. They note that Australia’s major miners would still make healthy profits at these levels due to their low cost of production, and with cost base advantages in other commodities such as coal, copper and gold.

Credit Suisse also sees a correction on the horizon, with the AFR quoting their strategist as saying last week “We have been bulls on the Aussie commodity stocks for over a year. However, after the strong run we think it is time to further trim our long position. At our peak we had five commodity stocks in our 12 stock long portfolio. This came down to four when we took profits on Fortescue a couple of weeks ago. Today, we trim further and take profits on South 32.”

It is certainly fair to say that resource stocks have had a good run since the start of last year, but also that this needs to be placed in the context of a significant pullback in 2015, and prior. I also think that position will be very different if the consensus analyst fraternity is wrong, and commodity prices weaken slightly but generally hold the line. The risk for many financial institutions is that they remain underweight and the sector has another surge to the upside.

South32 broke out to the upside last week, and a further upward extension is probable in the weeks ahead