POSTED BY ANGUS GEDDES

Good morning,

It was a familiar run into the close for US stocks on Tuesday with the indices staging a sharp selloff in the closing hour of trade. Led by a slumping Nasdaq, technology stocks dragged the broader market lower with Facebook leading the decliners after it was announced that CEO Mark Zuckerberg is to appear before Congress. Trade worries also continued to weigh on sentiment, with this time concerns mounting that chipmakers and software companies would be caught up after reports that the White House would be targeting Chinese investments within the US tech sector. The Dow Jones closed down 1.43%, the S&P500 lower by 1.73% and the Nasdaq dropped 2.93%.

Dow Jones

As I wrote yesterday, I see the markets fear of a trade war rescinding as it becomes clearer what the Trump Administration’s objectives are – namely a negotiated outcome between the relevant parties. Trump must be seen to delivering on electoral promises, but he is pro-business and his Administration will therefore seek to mitigate a trade war and we should see the rhetoric begin to taper off.

We saw this over the weekend following sharp losses on Wall Street when Steve Mnuchin sought to calm the markets. We can probably expect more of the same from the White House if the volatility continues on Wall Street.

Today was more about the FANG stocks coming under pressure, led by the derating in Facebook. The leadership group of tech companies that have led the market for so long is suddenly being questioned by the market. With Facebook suffering significant technical damage in recent weeks, other leading IT names have been caught up in the ensuing selloff.

For companies such as Netflix (which is yet to generate substantial earnings and does not have a fortress like balance sheet) the decline today was more severe, with the stock down by more than 6%. Tesla lost over 8% as investors flocked to less risky areas of the markets. Incidentally with Tesla, key support was broken definitively today, with the stock down more than $100 from the peak. We are therefore beginning to see the leadership group of names change in the US IT sector as the market returns to focusing on balance sheet strength and cash generation.

I still however believe the current fear will soon give way to fundamental factors after the US indices closeout a torrid quarter and a deep correction. The next phase, which commences shortly after the Easter holiday, is the Q1 quarterly reporting.

Once again fundamentals will be at the forefront as companies report earnings against what has been a solid three months for the US and Global economies. This should begin to dominate the mindset of investors over the next month and distract from the White House trade agenda.

And as I highlighted on Monday, the price earnings multiple for the S&P500 is now around 16X, which is attractive when considering the upbeat condition of the economy and underlying growth momentum.

But near term, the question on everyone’s mind is just how low can the SPX go?

As the US indices do a “double take” and approach the February bottom for what is shaping up to be a significant retest of the lows, the lower price earnings ratio and overall valuation for the S&P500 will sharply come back into focus.

Unless you think that corporate earnings are about to head off a cliff, the market should find a bottom soon. While today’s price action was once again disconcerting, I remain of the view that valuation, earnings momentum, and the robust economy will prove to be the mitigating factor for the stock market next month and the catalyst for the end of the correction when the reporting season gets underway.

Amid individual movers, Facebook shares declined 5% taking the recent slide to 22% from peak levels as analysts have lowered their price targets in the wake of the data scandal. This weighed on Google-parent Alphabet, which was down 4.6% in early afternoon trading, although it has justifiably held up better than Facebook after the data security news broke recently. Baidu shares slipped a more moderate 2% as demand is expected to be very strong for the upcoming IPO of its video streaming unit. More on that later.

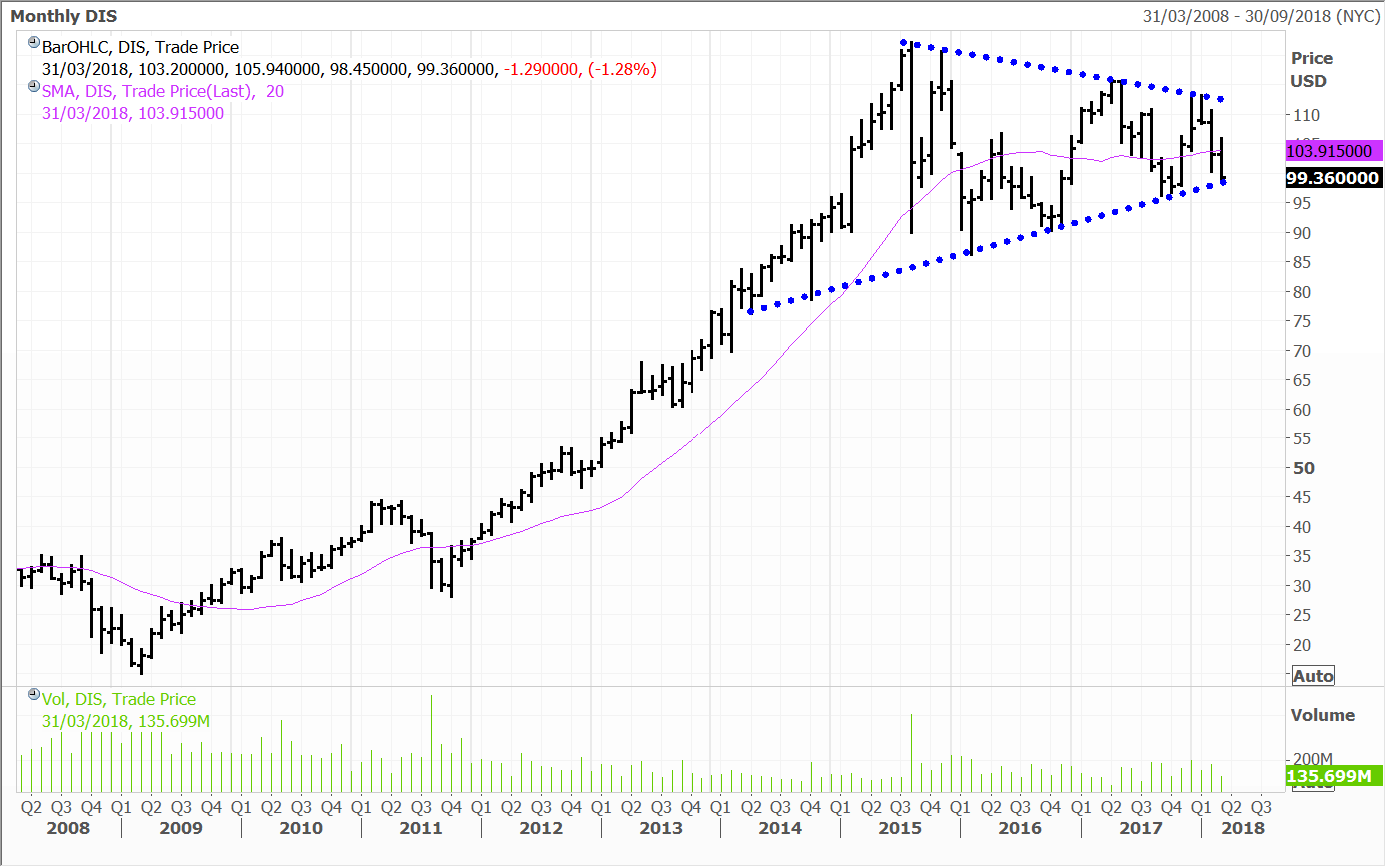

Walt Disney shares were effectively flat most of the day closing down 1.28% into the end of session. The box office run of Black Panther has been incredible. Last weekend the movie grossed $630.9 at the domestic box office alone surpassing the $623 million tally of The Avengers. And on that note, Avengers: Infinity War is due to hit cinemas in less than a month. When Disney begins to stream these brands next year on a subscriber platform, Wall Street is bound to recalibrate the value of Disney in my view. I think this is what Rupert Murdoch sees.

Disney will likely emerge with a formidable streaming offering to compete with Netflix next year, particularly with a huge brand portfolio and back catalogue post the FOX merger. Disney sells on multiple of just 14X and has a market cap of $150 billion. This contrasts with Netflix that has a market cap of $140 billion, little in the way of earnings and considerably less revenues than Disney.

Walt Disney

European stocks rebounded from one-year lows in trading Tuesday and as with other regions it appears cooling tensions on the trade side were supportive. The pan-European Stoxx 600 gained 1.21% for the day, while the Euro Stoxx 50 index of eurozone blue-chip stocks gained 1.17%.

Travel technology expert Amadeus IT gained 1.4%, while automakers BMW and Volkswagen advanced 1.6% and 2.9% respectively. Heidelberg Cement tacked on another 2.4% after last week reporting record revenues for 2017. Banks in the region were generally higher, with the likes of Bankia, BNP Paribas, Caixabank, Credit Agricole and Credit Suisse up between 0.3% to 1.3%.

The FTSE 100 closed 1.62% higher Tuesday as trade tensions eased. Plumbing and heating supplier Ferguson jumped 6.7% after it reported strong trading in the United States, which accounts for most its business. The company will issue a special dividend to shell out the expected proceeds from its sale of Stark Group.

BHP Billiton added 1.8% in trading, while Glencore surged 3.2%. Budget airlines easyJet, Dart Group and Ryanair gained 1.5%, 2.7% and 0.4% respectively. On the other side of the coin, fashion company Superdry tumbled 6.6% on news that founder Julian Dunkerton is leaving the business.

A willingness to negotiate between Chinese and American authorities on trade helped Asian stocks to a higher close Tuesday. In Japan the Nikkei surged 2.65% to its strongest day since 2015 as the yen weakened for the second trading session due to an improved risk appetite from investors. Dividend reinvestment was also a feature. Technology stocks and cyclical stocks made a strong recovery after taking a beating last week.

Construction machinery maker Komatsu surged 5.1%, Panasonic gained 5.0% and Sony advanced 3.0%. Touch screen technology leader Nissha Co jumped 4.6%, Truck maker Hino Motors added 2.8% and energy company Inpex advanced 2.9%. Industrial robotics experts Fanuc and Yaskawa Electric closed 1.8% and 2.9% higher respectively. The megabanks Mizuho, Mitsubishi UFJ and Sumitomo were also strong, with gains ranging from 2.1% to 3.3% on the day.

The Shanghai Composite advanced 1.05% and the benchmark Hong Kong index closed 0.79% higher.

In Hong Kong, property companies and technology stocks were some of the biggest gainers. China Overseas Land and Investment surged 4.4%, telecom giant China Mobile added 3.1% and social media conglomerate Tencent Holdings ticked up 1.3%. The Macau casino operators MGM China, Sands China and Wynn Macau all advanced between 1.2% to 4.3%. MGM, Sands and Wynn Macau are held in the Global Contrarian Fund. China Overseas Land and Investment, China Mobile, Tencent is a holding in the managed account portfolios.

In Australia the market bounced back on Tuesday, with the ASX200 closing up 41 points at 5,832. The SPI futures are pointing to this gain being reversed today as the ASX200 retests the Feb lows.

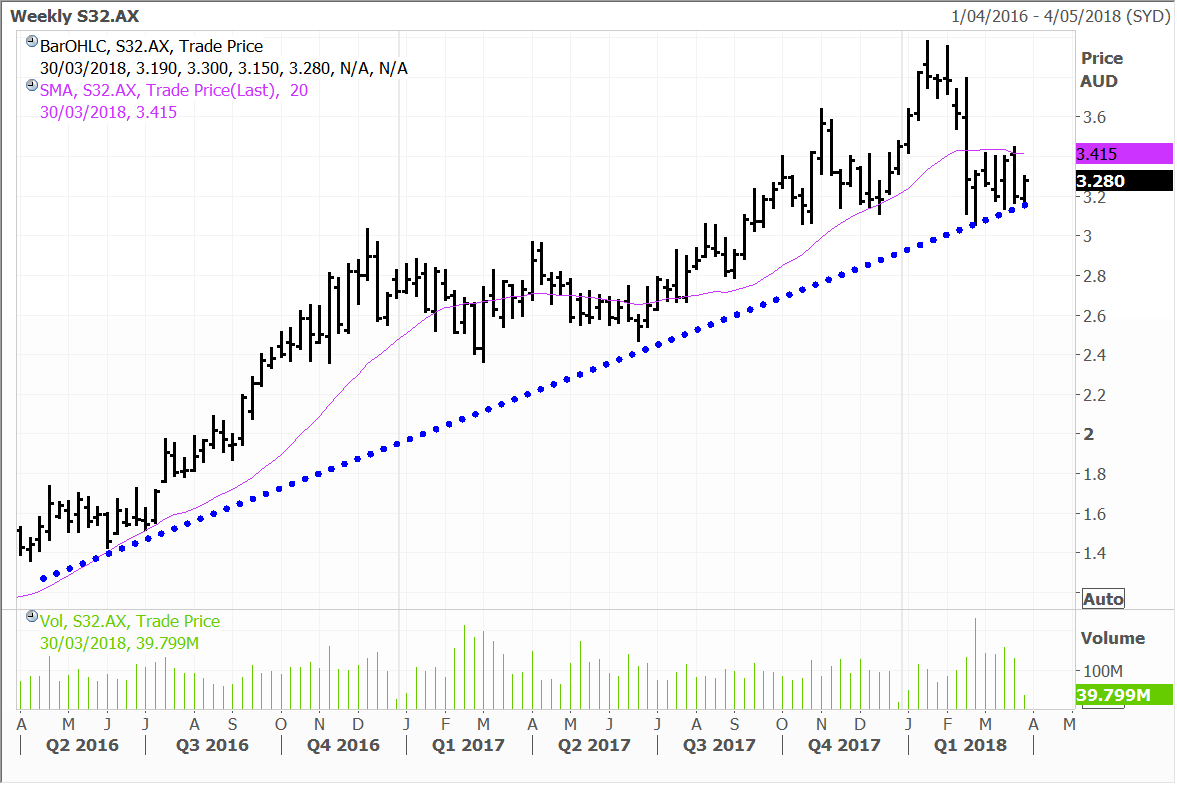

Resource stocks were well bid on Tuesday with South32 the standout, with a 3.5% gain. The shares have been consolidating since the retreat from the January highs, but remain a very strong play on further commodity price strength.

South32 has a strong production outlook, a robust balance sheet, and corporate activity is set to be another value driver with the proposed sale of its South African coal division. We hold South32 in the Global Contrarian Fund and the Australian managed account portfolios, with our analyst team rating the stock as a high conviction buy.

South32

The diversified mining heavyweights BHP and Rio were also higher, up 1.4% and 1.2% respectively. Rio has completed a further stage in its exit from coal, having agreed to sell its 80% stake in the Kestrel underground mine in Queensland for some US$2.25 billion to a consortium including EMR Capital and Adaro Energy. The deal requires approval from the FIRB and Queensland government.

Wynn Resorts is also benefitting from a strong rebound in Wynn Macau’s business, steady trading in Las Vegas and a couple of growth projects in the pipeline. The first is the water-themed ‘Paradise Park,’ adjacent to the company’s existing casino resort in Las Vegas. Wynn is also building a casino resort in Boston. The company broke ground in July 2016 and believes it will be a three-year project. The budget is over $2 billion, so it is a substantial investment.

Elsewhere Morgan Stanley upgraded Wynn Macau and MGM China price targets after revising forecast revenues and profits up significantly yesterday. Wynn Macau and MGM China. Both stocks are the two largest in the Global Contrarian Fund.

Bankers working on the IPO of iQiyi announced on Tuesday that the US$2.4 billion deal is substantially oversubscribed ahead of pricing scheduled to take place on Wednesday. iQiyi is Baidu’s video streaming unit that has been labelled the “Netflix of China”. Baidu intends to list iQiyi on the Nasdaq stock exchange. The deal has the potential to be the second biggest China-to-USA IPO after Alibaba raised US$25 billion in 2014.

“The deal has attracted an extremely high-quality order book and limited price sensitivity”, according to a banker close to the deal. He said: “There have certainly been plenty of Chinese deals that have had reasonably strong books that have not turned out to be home runs. So (the company and underwriters) will have to get the allocations and pricing right.”

iQiyi is selling 125 million ADR’s (American Depository shares) at US$17 to US$19 per share. The company could increase the number of shares or the price range, although China-to-USA deals generally stick to the original terms. Baidu and Hillhouse Capital will each buy US$200 million in the offering representing 17.8% of the shares.

iQiyi operates the biggest video TV streaming service in China. The business had 60 million paying subscribers at the end of February and in 2017 the company reported US$2.7 billion in revenue. Baidu’s shares were 2% lower on Tuesday and is held in the Global Contrarian Fund and in the Global and Asian managed account portfolios.

Baidu

Disclaimer: The Fat Prophets Global Contrarian Fund declares a holding in Baidu, Walt Disney, Bankia, Caixabank, Volkswagen, BHP Billiton, Fanuc, Inpex, Hino, Nissha, Sony, Mizuho, Mitsubishi UFJ, Sumitomo, MGM China, Sands China, Wynn Macau and South32.