POSTED BY ANGUS GEDDES

European equity markets were weak on Friday with the Stoxx 50 index closing 0.73% lower at 3,467. Euro strength continued to be a headwind for European stocks with the technology sector also selling off in sympathy over Amazon’s results. Eurozone economic confidence hit a new decade high in July with the Economic Commission’s reading up 0.1 points to 111.2. This is the best level since the financial crisis took hold in 2007.

Spanish economic output grew by 0.9% in the second quarter versus 0.8% in the first quarter. Spain’s economy is now reported to be back at the size it was before the credit crunch took hold in 2008. The stock market is still well below pre GFC levels, and I continue to think the Spanish stock market offers value and significant operating leverage to improving economic conditions. A breakout of the IBEX above 11,000 is only a matter of time.

Spain’s recovery is being driven by a virtuous cycle of rising wages, more jobs and lower unemployment and increasing consumer demand. We are heavily represented with Spanish stocks in the Fat Prophets Global Contrarian Fund and in our Managed Account portfolios, holding names such as Bankia, Bolsas Y Mercados and Telepizza.

In the UK the FTSE 100 closed 1% lower at 7,368 with the two tobacco stocks in the index selling off sharply. The US Food and Drug Administration has said it will start looking at the arguments in favour of cutting back nicotine in cigarettes. The latest survey of economic confidence in Britain showed a decline to the lowest point since the Brexit referendum. The GfK consumer confidence index fell to -12 in July from -10 in July.

International companies in the news

HDFC Bank Ltd on Monday reported a 20.2% rise in its net profit for the June quarter on higher interest income. Net profit rose to Rs3,893.84m in the three months ended 30 June from Rs3,238.91m a year earlier which was in line with expectations. Net interest income (NII), or the core income a bank earns by giving loans, increased 20.4% to Rs9,370.74m from Rs7,781.44m last year. Other income jumped 25.3% to Rs3,516.66m.

Speaking at a post results press conference, Paresh Sukthankar, deputy managing director, said that the bank continued to maintain a healthy loan growth rate, in both retail and corporate. While retail loans form 54% of the total book, Mr Sukthankar said demand was strong across the board on the corporate side, in trade finance and loan refinancing opportunities. Asset quality was the only blip in the fiscal first earnings, with the total increase in gross bad loans being around 60% in the agriculture loan portfolio.

“Recoveries from agriculture advances were impacted during the quarter by borrower expectations of farm loan waivers arising out of policy announcements in certain states. These loan waiver policies are in the process of being finalized and implemented. As a prudent measure, the bank has enhanced specific provision coverage for its non-performing agricultural advances” the bank said in a statement.

Sukthankar said as a prudent measure, the bank set aside more money to cover bad loans.

Provisions and contingencies climbed 23.5% to Rs1,558.76 crore in the June quarter from Rs1,261.80 crore in the preceding three months. On a year-on-year basis, it surged 80% from Rs866.73 crore. The provisions also include those for standard loans from certain stressed sectors such as telecom and steel.

“The bank has maintained that there could be some stress on the agri loan portfolio going ahead also. However, given that the core loan portfolio has remained largely stable and growth rates have picked up again, the earnings visibility remains fairly stable for the bank”.

HDFC is a core holding in the Fat Prophets Global Contrarian Portfolio and the Global Opportunities and Asian Managed Account portfolios.

Beating the street

Shares of Chinese search giant Baidu jumped 9.4% in trading on the Nasdaq Friday, after “beating the street” by a huge margin. Following on the heels of a blowout second quarter, net profit surged 82.9% year-on-year to RMB 4.41 billion (US$651 million). That was approximately 50% higher than the median analyst projection according to Bloomberg data.

We were looking for a return to headline revenue growth in the core search business and Baidu certainly delivered last week. It was also the quality of the beat that impressed, with the company showing traction in mobile and artificial intelligence (AI). The company’s core advertising business has also bounced back due to a much higher quality customer base, which led to less spending on promotional activities and higher operational profits.

Baidu announced a partnership with PayPal that allows Baidu Wallet users to link those wallets to PayPal to make online purchases outside of China. For PayPal, it improves access to the world’s biggest mobile payments market (China). And not wanting to be in the position of playing catch-up again, Baidu is betting big on AI to be at the forefront in this exciting new space.

Baidu is the largest holding in the Fat Prophets Global Contrarian Fund, and is also a significant holding in the Global Opportunities and Asian Managed Account Portfolios. Baidu has been a laggard relative to major rivals Tencent and Alibaba in mobile, so the improvement in its mobile monetization is a major positive.

Discussing the company’s future strategy, Robin Li, Baidu’s Chairman and Chief Executive Officer stated, “In the second quarter, Baidu announced our new mission to make a complex world simpler through technology,” and added “To achieve our mission, we will execute on two strategic pillars: to strengthen our mobile foundation and lead in AI. We will use AI as a fundamental driver to elevate our current core business, specifically our core products of Mobile Baidu, search and feed. In parallel, we will continue to build out our newer AI-enabled initiatives through an open platform and ecosystem approach to capture long term economic opportunity.”

Although much of AI’s monetization potential is in the future, Baidu is leveraging its expertise in the space to improve search and advertising placement to bolster revenues now.

Baidu’s chief operating officer and a leader in the AI space, Qi Lu, said on a conference call with analysts that, “with regard to our core search product, particularly using AI technology to increase the core aspects of the product which is relevancy. There’s indeed plenty of opportunities to increase the overall relevancy of a search experience, particularly as we increasingly personalize our search processes.”

“One of the important areas we see we can grow, not only the search quality in terms of relevancy but also use that to expand the scope of what search can offer. So search can become more and more personalized over time by using AI as technological foundation to drive those growths. On the monetization side, indeed, we see headrooms by using AI technologies to continue to improve the economic yield. Particularly by leveraging more conversion data, using deep learning.”

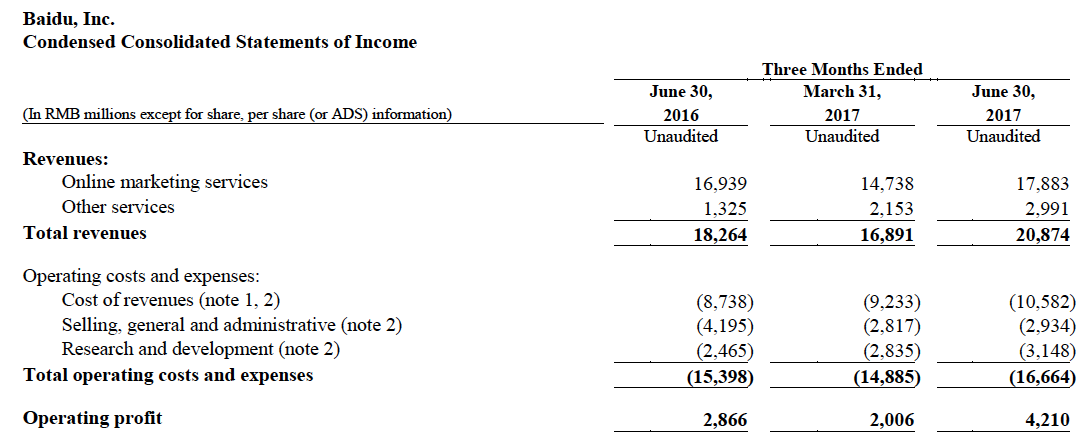

2Q17 headline numbers

Moving onto the quarters key numbers briefly, total revenues in the second quarter of 2017 came in at RMB 20.87 billion ($3.08 billion), marking a 14.3% increase on a year ago. Positively, the component generated from mobile increased from 62% in 2Q16 to 72% in 2Q17.

It was the second consecutive quarter of year-on-year growth after some weaker quarters in 2016 when the company faced two headwinds. The first headwind was the absence of a contribution from the online travel business, Qunar, which was deconsolidated from Baidu’s financial accounts in late 2015.

Secondly, Baidu’s core online marketing (advertising) business was impacted by the aftermath of a medical scandal. Sadly, a young Chinese man with cancer died last year after ordering experimental medical treatment that was listed amid Baidu’s search results. The ensuing scandal ultimately resulted in authorities imposing stricter regulations on advertising and saw Baidu tighten internal vetting standards for advertisements.

Although that weighed on the results for a while, with lower quality advertisers shaken out, the overall quality of the advertising business has improved. Online marketing revenues in 2Q17 were RMB 17.88 billion, up 5.6% year-on-year. Baidu had fewer online marketing customers, with 470,000 representing a 20.9% decline, but revenue per customer was up big time, surging 32% to RMB 37,500.

This has helped Baidu rein costs linked to its ad business, with selling, general and administrative expenses of RMB 2.93 billion down 30.1% year-on-year. Some other expenses are still on the up, such as R&D and content costs, but overall, Baidu has been exhibiting better cost discipline in recent quarters by narrowing its focus on fewer areas such as search, AI, mobile and the cloud. Operating profit was up 46.9% year-on-year to RMB 4.21 billion.

Source: Baidu

As stated earlier, Baidu’s net income hit RMB 4.41 billion ($651 million), representing a jump of 82.9% year-on-year, with this partly due to a weak result a year ago. Diluted earnings per ADS (the American listed instrument) were RMB 11.31 ($1.67), which easily beat the Wall Street consensus estimate and the RMB 6.57 figure from a year ago. Non-GAAP net income increased even more, effectively doubling (+98.4%) year-on-year to RMB 5.57 billion ($822m).

Baidu was also upbeat about the upcoming quarter, saying it expects total revenues to at a year-on-year pace of between 26.7% to 30.1%.

Disclosure: The Fat Prophets Global Contrarian Fund declares a holding in Baidu, HDFC, Bankia, Bolsas Y Mercados and Telepizza.